If you’re living in Japan and looking to invest and save on taxes, you’ve likely come across two powerful tools: NISA (Nippon Individual Savings Account) and iDeCo (individual-type Defined Contribution pension plan). Both offer excellent tax benefits, but they serve different purposes and have different rules.

So, which one should you choose?

Let’s break it down, compare the two, and help you decide based on your personal goals and lifestyle.

| Feature | NISA | iDeCo |

|---|---|---|

| 🎯 Purpose | Tax-free investing | Pension savings |

| 💰 Tax Benefit | No tax on gains/dividends | Contributions are tax-deductible + tax-free gains |

| 🔓 Withdrawal | Anytime (no penalty) | Age 60+ only |

| 💸 Max Contribution | ¥1.2–3.6M/year | ¥14,000–¥68,000/month |

| 🧑🤝🧑 Eligibility | Age 18+ | Age 20–65 with income |

| 📈 Product Types | Stocks, ETFs, mutual funds | Mostly mutual funds |

So, what’s the good and the bad of each of these plans?

| NISA | iDeCo |

|---|---|

| 🟢 Pros Flexible withdrawals Easy to start Tax-free gains Ideal for mid- to long-term investing | 🟢 Pros Contributions reduce taxable income Tax-free gains Builds retirement savings automatically |

| 🔴 Cons No tax deduction on contributions The tax-free period has limits (5–20 years) | 🔴 Cons Locked until age 60 Limited product options Setup can be complex |

| Where are you in life? | Recommended Plan |

|---|---|

| 🧑🎓 Young beginner | NISA |

| 🧑💼 Full-time worker or self-employed | iDeCo (or both) |

| 👵 50s & approaching retirement | NISA (maybe both) |

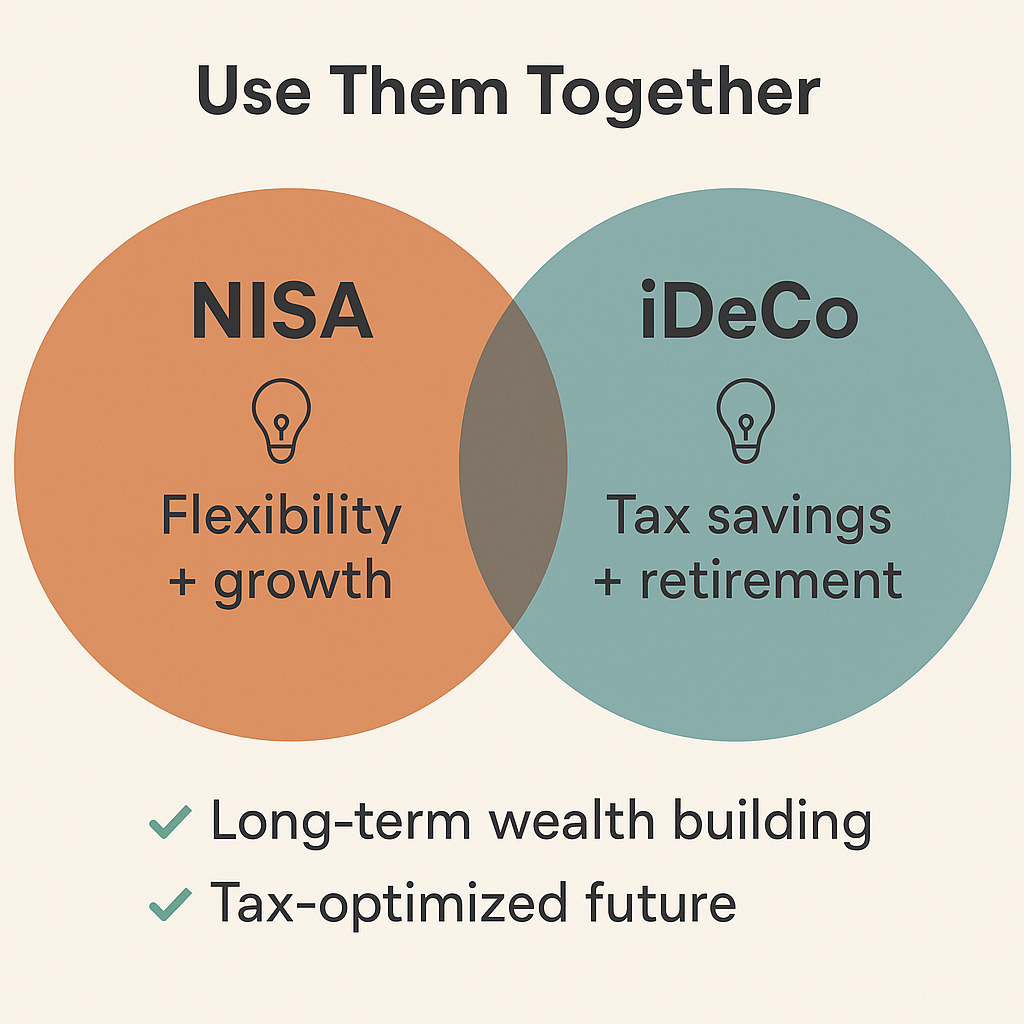

| 💰 Wanting full tax efficiency | Use both |

“I want to access my money anytime.” → NISA

“I want to lower my taxes now.” → iDeCo

Each system has its strengths, and the right choice depends on your age, income level, and financial goals. If possible, combine both to take full advantage of Japan’s tax-saving systems.

If you’d like help setting up your NISA or iDeCo account, or want to learn how to build a tax-smart investment plan in Japan, feel free to reach out or comment below!

Leave a Reply